Fojtasek Case Report

Case: Accel Partners VII

Date: Jan. 25, 2022

Managing Partner: Helen Hsu

Partners: Jaden Faunce, Radha Panchap, Isshaa Tusnial

Date: Jan. 25, 2022

Managing Partner: Helen Hsu

Partners: Jaden Faunce, Radha Panchap, Isshaa Tusnial

Executive Summary

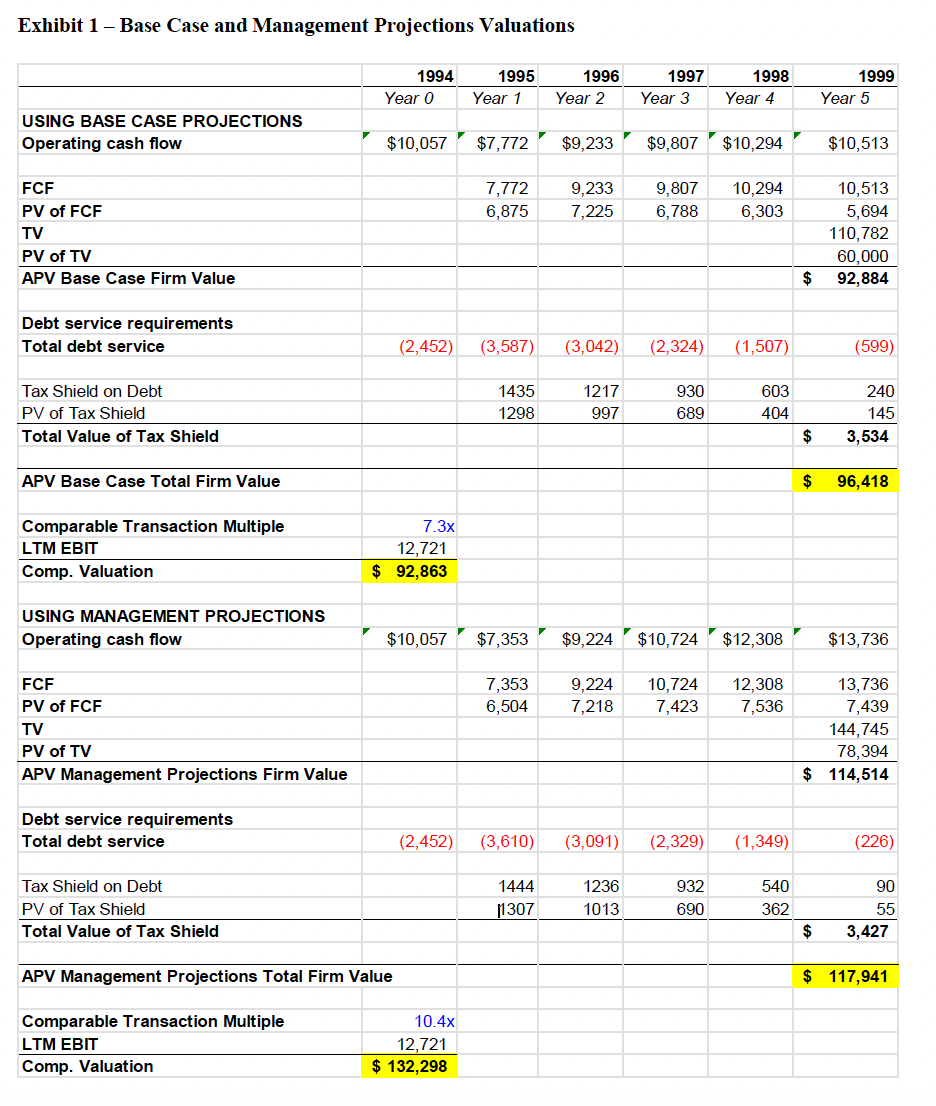

The Fojtasek family has many options for the future of their business, ranging from buyouts, a levered recapitalization, and the offer from Heritage Partners. Using both an Adjusted Present Value and a Comparable Transactions analysis, we determined a value range for The Fojtasek Companies, “the business,” under base case assumptions and management projection assumptions. The value range for the business under base case projections is between $92,863,000 and $96,418,000. Under management projection assumptions, the value range for the business is between $117,941,000 and $132,298,000 (Exhibit 1). We think that given the nature of the business and the macro environment, the base case assumptions provide a more realistic valuation range. Furthermore, using the valuations above, the materials provided by Heritage Partners, the history of The Fojtasek Companies and its family dynamics, we recommend that both Heritage Partners and the Fojtasek family undertake the proposed transaction.

Valuation

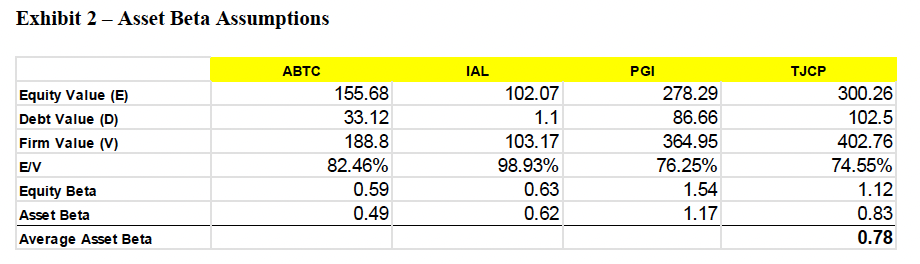

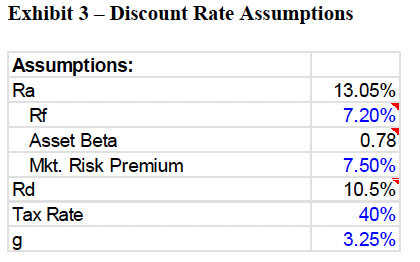

In the Base Case scenario, the comparable transaction valuation is a few million dollars more conservative, whereas in the Management Projection scenario the adjusted present value method of valuation provides the more conservative estimate. For the APV valuations, we used a few assumptions that helped guide our calculations. For our discount rate of free cash flows, assumptions are as follows: the asset beta used is derived from an average of similar public companies’ asset betas (0.78) (Exhibit 2), the risk free rate is equal to the yield on the 10 year treasury (7.20%), the market risk premium used is the standard market return (7.50%). For terminal value calculations, the long term growth rate is in line with GDP growth (3.25%). In order to discount the tax shields, we used a corporate tax rate of 40% and a discount rate equal to the prime rate plus 1.5% (9% + 1.5% or 10.5%) (Exhibit 3). Under these assumptions for the APV method, we derived a base case firm value of approximately $96.5 million and a management projection firm value of approximately $118 million.

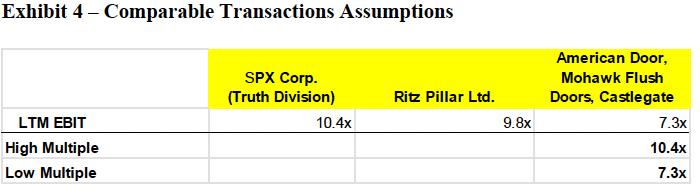

When performing the comparable transactions valuation, we first chose the firms that underwent acquisition which we thought were most closely related to Fojtasek, then we removed any outliers, and finally took a range of LTM EBIT multiples from the selected transactions. Using these principles, we got a LTM EBIT range of 7.3x on the low end, and 10.4x on the high end (Exhibit 4). Using 1994 real EBIT of $12,721,000 we calculated a base case comparable valuation of approximately $93,000,000 and a management projection comparable valuation of approximately $132,000,000.

Recommendation

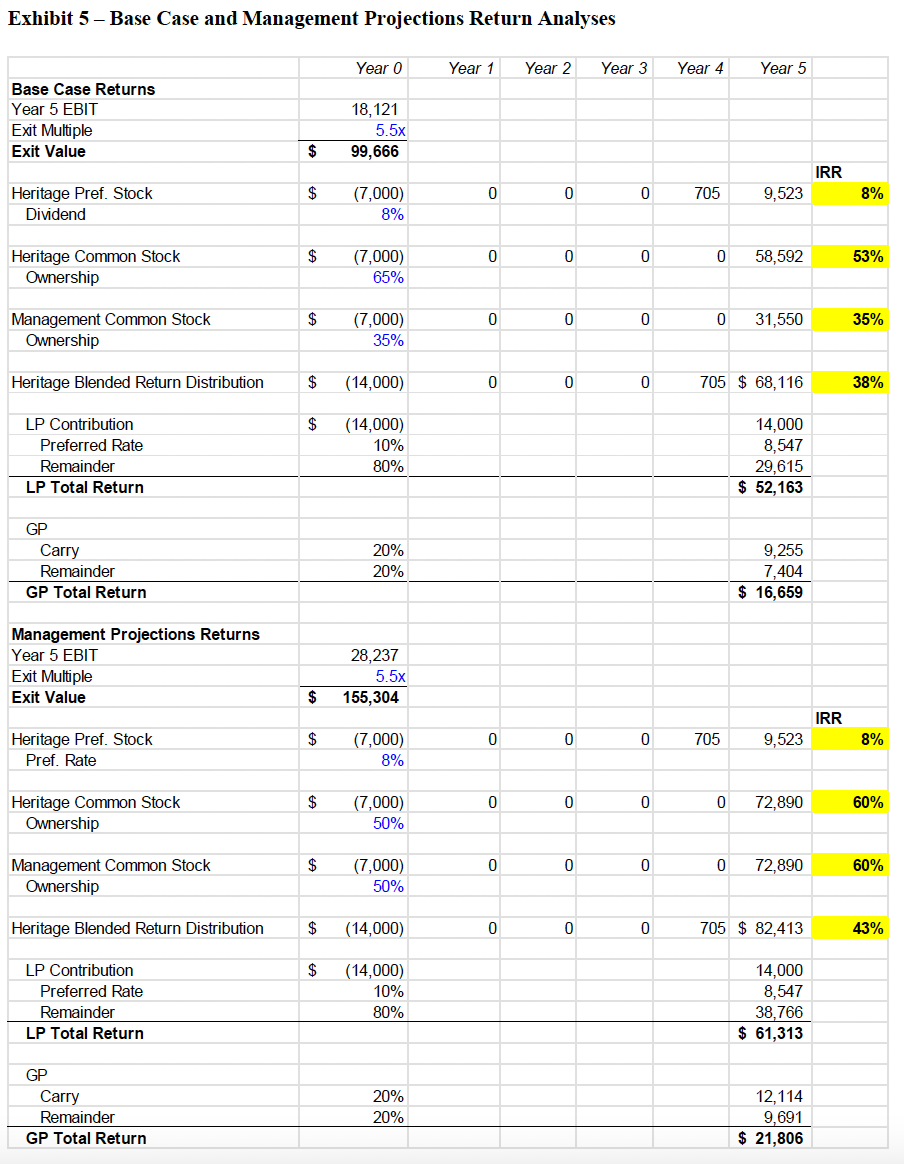

After performing a return analysis, it is clear to us that the Heritage Partners offer provides a win-win situation for all parties. Under the base case scenario, we see Heritage’s blended IRR equal to 38% and under management projections, they walk away with a 43% blended IRR. Furthermore, base case distributions to LPs total about $52 million with another $16 million going to the GPs. Under management projections, these numbers rise to $61 million and $22 million respectively (Exhibit 5). Not only is this a very attractive investment from an economic and financial perspective, but both sets of operating assumptions (and covenants with respect to targets met – Heritage will own 65% of the business if only base case assumptions are met) allow for Heritage to maintain attractive IRRs at exit. This deal also follows their investment thesis very closely regarding industry, size, and dynamics of the owner/family behind the business.

In regards to the Fojtasek family, although the offer is a few million dollars less than some of their previous offers, this deal still provides a very attractive return, and also gives them a “second bite of the apple” with the inclusion of rollover equity for management and family members. This exposure to a second liquidity event more than makes up for the smaller upfront consideration. Furthermore, the rollover equity portion of the deal accomplishes two more important factors that were weighing on the Fojtasek company. First it allows for those family members who want to stay involved in the business to actually stay involved, and second, the deal is structured so that the family remains some control and decision making power in the business during Heritage’s tenure. Those family members and managers who choose to reinvest into the new company will see an IRR of 35% under the base case and an IRR of 60% under management projections (hard to beat elsewhere). At the sale of the business in five years, those who chose to reinvest will realize a gain of $31 million under the base case and nearly $73 million under management projections (Exhibit 5). We believe that not only does the Heritage offer provide a win-win option, but incentives are strongly aligned with both parties so that they cooperate, work together, and achieve management projections to ensure that they get the most value possible (family and management who reinvest have skin in the game and will lose some value if management projections are not achieved, and Heritage also benefits more in their GP compensation and in regards to their reputation when management projections are achieved.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}